Comments Off on Reflecting and Projecting 2023 – 2024

As humans, it is natural for us to take things for granted. Our children will stay young forever. A business will continue on its current growth trajectory. 2023’s rapidly changing interest rate environment served as a reminder that things can change quickly. On March 17, 2022, the federal government set out to slow down an economy that was growing at an unsustainable rate. The federal funds rate rose from 0.25% to 0.50% in March 2022 to 5.25 to 5.50% on July 26, 2023 which represents the last rate hike (https://www.forbes.com/advisor/investing/fed-funds-rate-history/). That’s 500 basis points in 16 months! Rapidly increasing the federal funds rate achieved the government’s goal of slowing inflation. The speed of change was rapid, being the fastest in multiple decades, and sent shock waves throughout the commercial real estate world. Some of Black Diamond Realty’s observations are captured in the bullet points below.

Buyers were forced to adjust their internal underwriting to account for higher borrowing costs, due to higher interest rates, which ultimately led to rising cap rates.

Sellers are also forced to adjust value expectations when evaluating their assets and pricing to meet required DSC for Buyers of their assets (making it a bankable deal). Sellers are slow to adjust to a changing economy. Human nature protects our psyche resulting in most sellers reluctancy to accept the fact that asset valuations from mid-2022 are no longer an accurate representation of today’s market value.

The buyer-seller gap was wide at the beginning of early 2023 but slowly shrunk. Like many things in life, time heals wounds or, in this case, narrows the buyer-seller value expectation gap.

Banks are quick to adjust pricing and risk tolerance guidance and adjust required DSC levels and reprice assets.

Banks struggle with nonperforming assets and collections.

Metro markets often rise faster than tertiary markets and, therefore, tend to fall faster when economic conditions adjust. The markets Black Diamond Realty services experienced a slowdown in activity but it was much less profound than many metro markets consuming national media.

Greater increase in creative deal structures including seller financing.

Higher interest rates make leasing a more attractive option for some businesses. In comparison to sale volume, leasing activity has experienced increased transactions across most sectors of commercial real estate.

High borrowing costs, combined with increased labor and material costs, have resulted in a significant slowdown in new construction starts. This is a national trend in most markets.

Land sales have slowed. Higher interest rates and increased construction costs make it more difficult to “pencil” returns that meet developer hurdle (internal return) rates.

Less individuals can afford to buy their “dream home” because of rising home prices and rapidly changing interest rates which has resulted in many potential buyers sitting on the sidelines and renting longer. Market rents have continued to tick up in most markets helping to create greater demand in CRE’s multifamily sector . Market inventory continues to be the key struggle leading to lower transaction volume this sector.

2023’s theme was rapid change. What will 2024 look and feel like? Predicting the future is impossible, but national trends and experience allow us to make educated guesses. Please bear in mind you should always complete your own due diligence before making an investment decision. Black Diamond Realty’s 2024 predictions are as follows:

The Federal government is anticipated to lower interest rates three to six times throughout the year. BDR anticipates four lowering events with a final result between 100 to 150 basis points.

Election years usually create uncertainty and fear which causes many investors and businesses to adopt a holding pattern. Declining interest rates should create a market buzz but uncertain political outcomes will soften 2024’s activity. In comparison to 2023, greater CRE deal volume is anticipated.

Combined with high bank CD and money market rates, 2023’s slowdown in CRE activity has led to pent up demand with a lot of “powder” sitting on the sidelines. Cash is, once again, king/queen. “One person’s demise is another’s potential treasure.” Many adjustable and/or maturing loans will present buying opportunities over the next 12-24 months.

Banks will be quick to move nonperforming/uncollectable assets off their books. This will create opportunities for buyers to pick up properties at a discount…timing and connections will be key to buying up these assets.

Office assets, overleveraged real estate and properties financed with short-term debt all face headwinds in 2024. Distress, leading to buying opportunities, is anticipated across these categories.

User demand for industrial/logistics, retail and residential is anticipated to remain strong.

Cash buyers and international investors are anticipated to be more prevalent.

Banks will continue to tighten their lending belts and stress properties at higher interest rates (8-9%). Debt service coverage ratio (DSCR) levels will continue to be higher than pre-COVID levels. Most banks will require a 1.25 DSCR

We often joke Black Diamond Realty is not a group of magicians. We are skilled CRE professionals whose job is to maximize exposure, navigate complicated processes and provide sound consultative investment and decision-making guidance based upon experience. We are in the commercial real estate trenches every day. We do not sell homes.

Diversifying investments, pursuit of passive income, filling a void in your portfolio’s performance (leasing) and liquidating an asset to meet long-term goals are all reasons to contact our Black Diamond Realty team. Call our team of experts today to set up a consultation. We look forward to serving you in 2024 and beyond.

Article by:

David Lorenze, CCIMPrincipal, and team.

Comments Off on Reflecting and Projecting 2022 – 2023

Congratulations! You just rode one of the wildest rollercoasters the modern economy has ever experienced. Roughly one year ago, experts predicted interest rates would begin ticking up twenty-five to fifty basis points, with a target of 4.5 to 5% interest rates. The goal was, and still is, to fight record high inflation (9.1% in June 2022; a 40-year high). Many projections were far off, including ours. In today’s market, a 4.5 to 5.0% interest rate on a deal is unheard of and would make investors drool. As we enter a new year, we are looking at the prime rate hovering in the mid sevens; that’s 7.5%! This marks a 400-basis point increase in the past nine months.[i] Last year experienced the most aggressive economic tightening campaign in over three decades. So, how does that affect commercial real estate?

Rising interest rates put downward pressure on valuations. Financial institutions, including regional and national banks, typically want to achieve a 1.20 to 1.25 debt-service coverage ratio (DSCR), meaning 20%-25% of a project’s cash flow is available to pay current debt obligations. When the cost of borrowing funds increases, meeting required DSCR ratios is more difficult, and a buyer cannot afford to pay as much value to a seller while still maximizing leverage (borrowing power). A buyer either has to come up with more capital to lower the loan-to-value (LTV) ratio or lower the offer price. Here is an example:

ABC Investment LLC has renovated an asset and wants to cash out to redeploy capital into the next project. You like the asset a lot. You offer full asking price – $1,250,000. A bank that requires an 80% LTV ratio (some banks will offer lower, say – 70-75% LTV) will result in you needing to borrow $1,000,000. Nine months ago (Q2 2022), you could have hypothetically achieved an interest rate of 3.65% (Black Diamond often saw rates between 3.25% to 4.00%). Amortizing $1,000,000 over 20 years at 3.65% interest results in a monthly payment of $5,876.97. Fast forward nine months (Q1 2023), and that same loan structure has changed drastically.[1]

As of December 15, 2022, the current prime rate is 7.5% in the U.S., according to The Wall Street Journal’s Money Rates table, which lists the most common prime rates charged throughout the U.S. and in other countries by averaging out the prime rate from the ten largest banks in each country. The federal funds rate is currently 4.25% to 4.50%. With that in mind, you can see how the “fed funds plus 3.00” rule of thumb plays out: 3.00% + 4.50% = 7.50%.[ii] At Black Diamond Realty, we would argue this rate is very conservative, as our experience has resulted in many regional banks willing to entertain deals at lower interest rates – with a 250 to 300 basis point spread in play.

Getting back to our example, your investment company’s new interest rate (7.25%; 275 basis point higher than federal rate) results in a monthly expense of $7,903.76. The difference between a 3.65% interest rate and a 7.25% interest rate is $2,026.79/month. The yearly difference is $24,321.48. In today’s market, let’s assume a regional multi-family asset comps out and sells at a 7% capitalization rate. Utilizing a 7% capitalization rate, the $24,321.48 yearly interest rate difference results in a downward value adjustment of $347,449.71 ($24,321.48 / 0.07). This ~$350K difference results in a seller/buyer “value gap.” Buyers are forced to react quickly because the capital markets respond within weeks, often days. Some buyers are struggling to find deals while sellers reassess their motivations to liquidate. Sellers are realizing they missed the market peak. Buyers are coming to the table with greater liquidity to meet DSCR (healthy, “bankable” deal) and bridge the seller gap.

The current market reflects the seller-buyer gap. On its own, this would be bad news for sellers everywhere. Fortunately for the market, supply and demand also comes into play. Like many things in our economy, construction materials (think Lowe’s, Menards, Home Depot) have experienced significant inflation in 2022. Construction expenses rose 13.7% since September 2021.[iii] Higher construction expenses, including excavation work, have resulted in lower nationwide new housing construction starts. Privately-owned housing starts in November were at a seasonally adjusted annual rate of 1,427,000. This is a 0.5 percent below the revised October estimate of 1,434,000 housing starts and is 16.4 percent below the November 2021 rate of 1,706,000.[iv]

The same trend is true across most sectors of commercial real estate. Higher material costs combined with higher costs of borrowing funds (interest rates) has resulted in a slowdown of new construction activity. We anticipate this trend to continue. Sticking with the multifamily sector, lower housing starts have resulted in increased rents and corresponding increased valuations. The same data shows a downward trend in construction costs during Q4, 2022 which is something to watch in 2023. So, what else can we expect in 2023?

Deals happen in all cycles of commercial real estate. Rising interest rates create downward pressure but, on the flip side, rising rents/income result in higher valuation. Do these two opposite effects counterbalance each other? The answer is specific to each commercial real estate sector (supply/demand) and the specific market. Depending upon the market, rising income is outpacing inflation which continues to push rents higher. The risk lies in the job market. Job loss and higher unemployment will eventually reduce consumer purchasing power and result in less demand for materials, goods and real estate. When unemployment rises, rent growth will be at risk for most sectors of commercial real estate. Our team is keeping a close eye on unemployment in 2023.

The ‘R’ word has been tossed around many dinner tables and watering holes across America. An economic recession occurs when GDP, which measures trade and industrial activity, declines in two successive quarters. Are we amid a recession? US Government courses reported that Quarter 3 of 2022 saw a 3.2% increase in GDP over the previous quarter.[v] This increase is welcoming news after two quarters of declining GDP. Some fear the data is artificially inflated due to the government’s easing of energy costs. The biggest challenge in reviewing federal government data is the lag. Most data lags at least three months, sometimes six, which means the Fed is making decisions based upon outdated information. What does the real estate market cycle forecast look like knowing this? Keep reading.

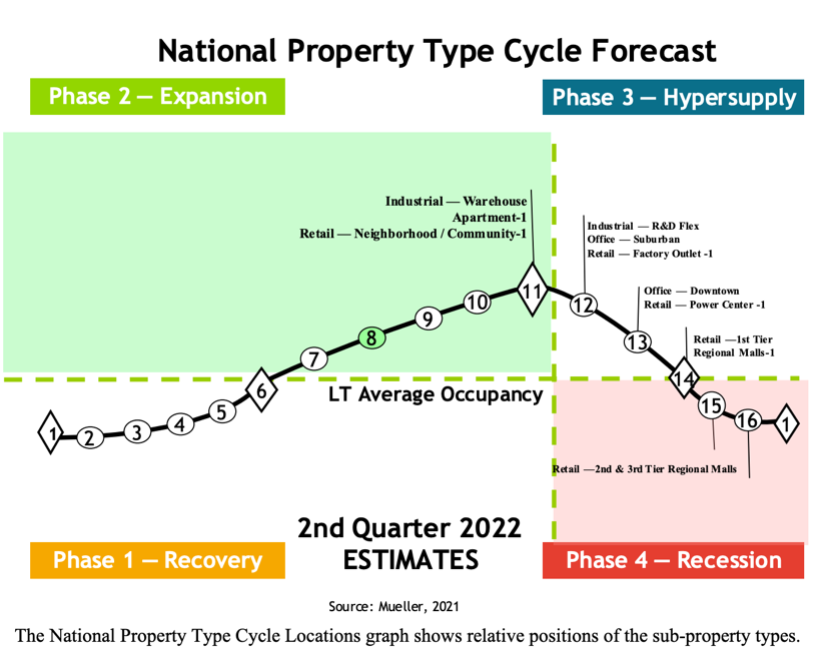

Real estate market cycles vary by sector and location, amongst other factors. Mueller’s[vi] forecasting model breaks down the real estate market cycle into four phases:

There are 16 total points along the horizontal axis. Points 1-11 are in phases 1 and 2 which represent a period of growth. Points 12-16 are in phases 3 and 4 which represent a period of decline. The four market cycle quadrants have varying characteristics. Phase 1, Recovery, is characterized by declining vacancy with little to no new construction. Negative rental growth to below inflation rental growth is expected during this part of the cycle. Phase 2, Expansion, is characterized by declining vacancy with greater new construction. High rent growth is common. Phase 3, Hypersupply, is characterized by increasing construction with continued and/or increasing construction. Rent growth remains positive but begins to decline. Phase 4, Recession, experiences increasing vacancy with more completions. Below inflation and negative rent growth is experienced during this part of the cycle. The Mueller report’s primary objective is to enhance investment decision analysis – to make investors aware of national trends.[vii]

Sector breakdowns are provided in the bullet points below with quick comments about the regional market. Keep in mind what is happening in New York City, NY is not necessarily a direct correlation to what is happening in Bridgeport, WV; hence several anecdotal comments from Black Diamond Realty’s perspective which are focused on the two core areas we serve: North Central WV and WV’s Eastern Panhandle. We recommend referencing the chart as you review the points below. Mueller’s data is the black bullet points. Black Diamond’s points are white sub-bullet points. In addition to this distinction (national trend – Mueller vs. Black Diamond), bear in mind Mueller’s chart lags by two quarters. The cycle has progressed along the bell curve over the past three to six months.

Point 11: Peak of Phase 2 – Expansion Cycle

Industrial – Warehouse

Remains strong throughout north central WV and WV’s Eastern Panhandle. For north central WV, keep an eye on oil and gas volatility/strength in 2023. For WV’s Eastern Panhandle, we are watching consumer confidence and retail strength.

Apartment

Remains strong in both markets due, in part, to the ability to push rental rates to counteract rising interest rates.

Retail – Neighborhood/Community

Still demand albeit at a slowing pace in both markets. Headwinds are forming which we believe will negatively affect all subsectors of retail.

Point 12: Beginning of Phase 3 – Hypersupply

Industrial – R&D Flex

Flex space has remained strong in both markets. North central WV has an undersupply of quality, newer flex space with docking capability. The Eastern Panhandle has consistently filled any new supply but it appears some headwinds could be forming (Hypersupply phase) where new product is taking longer to secure tenancy.

Office – Suburban

Demand still exists albeit at a slower clip compared to pre-Covid.

Retail – Factory Outlet

Point 13: Middle of Phase 3 – Hypersupply

Office – Downtown

Major metro markets have struggled post-Covid. In smaller/tertiary markets, he jury is still out on whether long-term leases will restructure plans as

Predicting future trends is nearly impossible. Market dynamics are complex and can shift quickly. Our team of experts has made some observations and anticipations for 2023. In no way, shape or form are we suggesting these “educated guesses” to be fact. Mere predictions are not indicative of actual future results. Please consult with your professional legal and financial advisors, complete your own due diligence and draw your own conclusions pertaining to the best financial moves for you.

Black Diamond Realty Predictions:

Real estate is considered by many as a great hedge against high inflation and a strong diversification play. Income producing assets are still warm, not hot, as an investment diversification play. Activity has cooled due to higher interest rates putting downward pressure on valuations. Ranking the sectors is difficult because there are so many factors (location, age, tenant, traffic patterns, surrounding amenities, etc.) but anticipated trends can be projected. In addition, there are several macroeconomic and microeconomic items we anticipate playing out in 2023.

Multifamily and industrial are anticipated to remain strong in the markets we serve. However, look for headwinds beginning to form within 12 to 24 months. Office is the weakest sector as evidenced by higher-than-average historical vacancy rates caused by lower demand created, in part, by work-from-home trends.

Tertiary markets with a core employment base of eds, meds and government jobs (considered recession resistant) will become more attractive to outside investors who are seeking a “safe place” to park capital. West Virginia has significant positive momentum as evidenced by the numerous basic employment announcements throughout 2022. Tertiary markets, similar to several growing areas in West Virginia (North Central, Eastern Panhandle), offer higher cap rates which are attractive to investors. Review Black Diamond Realty’s October newsletter article which compiles numerous statewide job announcements. Click Here.

One to two additional rate hikes in the first half of 2023. We anticipate a reversal, declining rates, starting as early as Q3 or Q4, 2023.

Can the government continue to service its debt at high interest rates? An economist who follows monetary policy, politics and global business much closer than our team will need to answer that question. What we know about monetary policy and our government’s current debt obligations is concerning, at best – downright frightening to others.

Black Diamond Realty anticipates seeing debt options with lower LTV ratios in 2023. Banks will adjust from offering 75-85% LTV to a range of 70-80% LTV.

Construction starts will continue to slow in most sectors. Multifamily and industrial may continue to expand in 2023 but high interest rates are putting downward pressure on construction starts.

Consumer confidence will slip. Challenging retail financial reports will follow. There will be heightened volatility in the stock market.

Our belief is that we are in the midst of a recession. It is either already here or quickly approaching. Government data lags by several months. Consumer confidence has declined during 2022.[viii]Inflation reached record highs in 2022 although it has been declining in recent months. Some believe the inflation decline is, in part, artificially enhanced by the government’s proactive action in releasing 1 million barrels per day of oil reserves. Energy prices will remain volatile especially if/when this strategy is lifted.

Black Diamond Realty is keeping a close eye on unemployment. When unemployment rates increase, consumer purchasing power will decline which will have a trickle up effect to GDP, negatively influencing most sectors in commercial real estate (most notably, retail).

For Black Diamond Realty, sales volume is forecasted to decrease while leasing volume will increase which should lead to leasing price increases in the high demand sectors (industrial and multifamily).

We recommend each party consults with its professional accountant, tax, and legal advisors to better understand the effects of market conditions and real estate transactions. Primary keys to successful investments are knowing the market, the numbers and market trends. Our professional team at Black Diamond Realty is an industry leader. Our company mission is to add value to the communities we serve. We look forward to consulting with you in 2023. Make it a successful investment year.

[1] It should be noted that interest rates can change drastically depending upon many factors, including the deal’s strength, the borrower’s financial strength (including investment and business experience), debt-to-liquidity ratios, and LTV.

The Morgantown Municipal Airport has the shortest runway in the state and, based on the number of flights, it is also the busiest. The airport’s lack of a longer runway acts as a hindrance to attracting and retaining additional corporate jet traffic and charter service.

Inclement weather, such as snow or fog, makes the already short runway even more difficult for jet operators to land at the airport. This means commercial planes and jets are less inclined to land at the airport. The goal of the runway extension project is to enhance and modernize the airport’s facilities to maintain current operations, recruit new business and improve safety at the airport.

Extending the runway will also provide a direct benefit to WVU athletics and will support the continued growth of the university, its partnerships and the local economy. That’s why the runway extension project is strongly supported by West Virginia University, and the administration has been pivotal in moving the project forward.

The benefits realized by the runway extension go beyond the city limits. That is why the project has also received support from local businesses, the Monongalia County Commission, Star City and the City of Westover.

Project Location

Address: Morgantown Municipal Airport, 501 Hartman Run Rd., Morgantown, West Virginia 26505

Project Budget

Funding for the project will include assistance from the FAA’s Airport Improvement Program (AIP). The FAA provides AIP grants to airports for projects that enhance airport safety, capacity and security or alleviate environmental concerns. The remaining cost will be funded by the City of Morgantown and the State of West Virginia. The project is expected to take at least five years to complete at an estimated cost of $50 million. Projected Expenditures | $50,000,000.00 * Last updated 01/22/20

See the Project Management and Project Timeline by clicking here

Glenn Adrian proposed interchange idea to commission. If you build it, they will come.

Sure, the line originated with disembodied voices and ghosts playing baseball in a cornfield, but the principle is a bit broader. For example, you could say if you build the proper infrastructure, investment, development, jobs and tax dollars will come. That’s precisely what Glenn Adrian is saying. Adrian, with Enrout Properties, is the owner of the Morgantown Industrial Park.

Adrian recently told the Monongalia County Commission and Delegate Mike Caputo, D-Marion, that after two years of back and forth with the West Virginia Department of Transportation and the governor’s office, he believes a deal is imminent that will allow various feasibility studies regarding a new I-79 interchange at the Harmony Grove/River Road overpass to begin.

He said building the interchange would not only make the park the only industrial site in West Virginia with barge, rail and interstate access, it would also remove the heavy flow of truck traffic that is funneled through Westover to access the 500-acre park via Dupont Road. It would also make the park far more attractive to potential investors.

Commission President Ed Hawkins called the proposal put forward by one of those potential investors “mind boggling.”

“We’re working very diligently with a significant clean manufacturer that wants to be here in the county … We’re talking about a 300,000 to 600,000 square-foot facility, up to 250 jobs and a lot synergies with WVU and the ag sciences and engineering departments,” Adrian said, adding, “This company, at its peak, will probably have 60 to 70 trucks a day. They’re a 24/7 operator. They cannot go here unless this becomes a reality.”

In order to help make it a reality, park ownership is working with the state on the creation of a second industrial park TIF district, the increment from which would expand water, sewer and road infrastructure to undeveloped portions of the park and reimburse the state for the estimated $20-$30 million interchange construction.

Both Adrian and the commission point to the $22 million construction of I-79 Exit 153 as proof that such an arrangement can work.

“The question is what’s the cost to the taxpayers, and in Mon County we don’t like running to Charleston and saying ‘We have this problem, what are you going to do for us?’ We try to bring solutions,” Commissioner Sean Sikora said. “That’s what happened with the first interchange. We found a solution to pay for it, and within a couple years it was paid off. It didn’t cost the taxpayers. It was all paid for from the increments out of the district. Same thing with this.”

The original industrial park TIF district was created in 2008. Adrian said the tax value of the park has gone from $26 million when Enrout purchased it, to between $45-$50 million. Add in the hundreds of miles of pipeline staged on the site for the now abandoned Atlantic Coast Pipeline project, that value jumps to approximately $90 million.

Sikora referenced a WVU economic study from 2019 that indicated the park as it’s currently configured has had a $1.1 billion impact on the state’s economy. Adrian said the interchange and park expansion would double that number over the next 10 years, according to projections.

Before any of that becomes reality, however, it must be determined if the interchange project makes sense.

“Interchanges like this are very arduous, A lot of studies have to go into it, which we’re going to pay for, but we’re very close to signing that collaboration agreement, Adrian said, adding, “We can draw all the pretty pictures we want, but the studies will determine the feasibility of this interchange.”

Comments Off on Cautious optimism in Monongalia County over Mylan Merger

Over the course of the next year, executives with the new company that will be formed from the merger between Mylan and Upjohn, a division of Pfizer, will be tasked with trying to reposition the company in a dynamic market that is facing a number of pressures.

Meanwhile, at least one elected official in Monongalia County does not want to just sit and wait for a decision on the future of Mylan’s current manufacturing plant near Morgantown.

“We are going to go on the assertive, be aggressive, promote West Virginia and promote how Mylan is so important to our community,” Monongalia County Commission President Tom Bloom said on WAJR’s Talk of the Town with Dave & Sarah on Tuesday.

The newly formed company — now being referred to as Newco — that results from the merger is expected to generate about $19 billion to $20 billion in revenue, with $1 billion in cost savings by pooling resources and trimming redundancies by 2023. Those synergies have some in the area anxious about the future of the Mylan plant and the jobs of about 900 union and 200 non-union employees.

United Steelworkers Local 8-957 represents about 900 employees at Mylan’s Morgantown plant. The Dominion Post aked what effects the Mylan-Upjohn merger might have in Morgantown, and President Joe Gouzd reiterated Tuesday morning what the union said on Monday: They don’t have enough information to comment at this point and they’re waiting to learn more.

But, Bloom is optimistic about the future. “They want to stay in the county and the CEO will be housed out of Pittsburgh, so that is a great sign for us,” Bloom said.

The new company will be led by current Mylan Chairman Robert Coury, who will serve as the executive chairman, and Michael Goettler, current group president of Upjohn, will serve as the CEO. The board of directors will include eight members designated by Mylan and three members by Pfizer, plus an executive chairman and CEO for a total of 13.

With the majority of the board having Mylan ties and the possibility of a growing generic drug market in Asia, Jared Hopkins, with the Wall Street Journal, believes Bloom’s optimism about the future of the Morgantown plant is not misplaced.

“What it [Mylan] gains with Pfizer is a commercial foothold in Asia as well as with their research and development,” Hopkins said on Metronews Talkline with Hoppy Kercheval. “That’s significant because China and Asia represent a huge opportunity for the pharmaceutical industry.”

According to Hopkins, business analysts have mixed feelings about the merger and the success of the future company.

“It’s been a little bit of a mixed bag. There have been analysts that have come out and said it makes strategic sense for Pfizer but potentially the math and numbers might not make it a successful deal,” he said.

“With Mylan, in talking with some analysts who have covered Mylan for a number of years, they’re saying this might make strategic sense but they’re a little skeptical given the history of Mylan over the last decade or so.” The generic drug industry is facing a number of pressures from manufacturers in India, which have entered the U.S. market, as well as companies aimed at connecting patients to medications causing new pricing pressures, according to Hopkins.

This has left companies such as Mylan and Pfizer trying to reposition themselves in the market and news of the merger put Monongalia County in a spot to reposition itself as well.

“We’re going to organize the delegates, the state senators, the city council members, let’s get everyone on board immediately to write a letter to Pfizer to welcome them to our community and explain how synonymous Mylan was to this community and how we’re looking forward to Pfizer being part of our community,” Bloom said.

Completion of the merger is expected sometime in mid-2020.

Comments Off on Economic Experts Tout Potential of Natural Gas Development

Growth in the state’s energy industries, along with the construction projects that come with it, offers many economic opportunities, but there is a balance to be had, as was demonstrated by speakers at the eighth annual Marcellus to Manufacturing Development Conference in Monongalia County.

John Deskins, chief economist for West Virginia University and director of the Bureau of Business & Economic Research, said the state’s economy is heading in the right direction overall, but added there are issues worthy of attention. “The 9,000 jobs we’ve added over the last two years are really concentrated,” he said. “This is part of the problem. The jobs we’ve added have been concentrated almost entirely in eight counties of West Virginia. Those eight counties are doing well. And we have 40 counties that are stable … some small growth, some small decline, but mostly stable.”

Despite improvements, Deskins said long-term problems remain. One is the state’s workforce participation rate, which is the lowest in the nation at only 54 percent of the state’s adults either working or actively looking for work, compared to a national average of 63 percent. He also pointed out that of the 9,000 new jobs, as much as 85 percent of them are in coal, natural gas or temporary construction work that is mostly related to natural gas. He said economic diversification is still a long way off. “We want energy to be strong,” Deskins said. “We want coal, gas and construction to be strong — obviously — but we have to have growth in other sectors like manufacturing, like tourism. This is the environment we find ourselves.”

Deskins said economic diversification is not only necessary for different types of businesses to flourish, but also to prevent a brain drain. For instance, he said when economic shocks occur, such as the decline of coal a few years ago, residents leave to find work elsewhere, and most of those who leave tend to be young people. This also leads to the vicious cycle of unemployment, despair and drug abuse. Deskins said the abundance of natural gas in Appalachia does present an opportunity to achieve economic diversification in view of the number of chemical and manufacturing industries that are drawn to cheap, plentiful and accessible feedstocks. “We have the opportunity to create tens of thousands of jobs over the next decade or couple decades,” he said.

Joe Bozada, chief operating officer of the Appalachia Development Group, said work on an Appalachian Storage Hub for natural gas to feed that economic diversification is underway. While the past year of development has been highlighted by the selection of Parsons Corporation as an engineering partner and securing loans from the U.S. Department of Energy, Bozada said the work on selecting underground sites to build the hub has also proceeded. He said that after negotiations with landowners, the list of sites has been narrowed down to five. Now the task, he said, is to further narrow that down to two sites — a primary site and a backup site.

He said the biggest risk to large-scale investment in West Virginia is a lack of suitable infrastructure. The Appalachian Storage Hub, when completed, will serve as a critical piece of that infrastructure, along with various pipeline construction projects, he said. “Our biggest risk is, essentially, why we exist,” he said, adding that the ultimate prize at the finish line is the 100,000 family-sustaining jobs the storage hub is projected to create via downstream development. Despite the promises of the storage hub, Bozada said other energy interests around the world aren’t just sitting back. They too are looking to expand.

He said U.K.-based INEOS has invested 3 billion euros into the construction of plastics manufacturing facilities in the Belgian port city of Antwerp — plants designed to use ethane derived from North American shale gas brought in by ships. Bozada said that while this is happening, American Ethane Co., which has Russian financing, is preparing to embark on a venture to supply Chinese markets with as much as $75 billion of ethane that would travel forth by sea through Beaumont, Texas, on the Gulf Coast, another hub of America’s petrochemical industries. He said volumes of that quantity represent an equivalent to the 100,000 jobs the creation of the Appalachian Storage Hub could provide.

Looking back to Appalachia, Long Ridge Energy President Robert Wholey said there are opportunities for business development in the remains of older industries that have since shutdown. He said one only needs to look across the Ohio River in Wetzel County to see an example. Located in Hannibal, Ohio, sits the leftovers of Ormet Primary Aluminum Corporation which is being redeveloped into a gas-fired power plant. The smelter, once the third largest aluminum smelter in the U.S., shut down in 2014, but development into a power plant started almost immediately after Long Ridge’s parent company, Fortress, purchased the property in 2017.

“It used as much power as the city of Pittsburgh,” Wholey said. “It went bankrupt because the power prices were too high. The terrible irony of it was that power was right beneath their feet.” Wholey said a particular advantage of developing such a site is the fact that much of the infrastructure is already in place, which can speed up the process and reduce some costs.

Between potential for growth in the energy and manufacturing sectors, coupled with technology and federal government operations, there are plenty of sound investment opportunities in the Appalachian region despite its challenges.

Such was the subject of industry and business development conferences held recently in Monongalia County. At the eighth annual Marcellus to Manufacturing Development Conference, Solvay Senior Vice President Wally Kandel said West Virginia has advantages in downstream industrial potential for its natural gas unique to other high-production areas around the globe.

He said that while the U.S. Gulf Coast remains a production and shipping powerhouse for natural gas, that region remains vulnerable to hurricanes and is far from the majority of its customers. Kandel said the decision to invest more heavily in the Gulf Coast was a sound one based on the technology and knowledge available in 2010. However, much has changed with the advent of horizontal drilling, and the advantages of the shale deposits in Appalachia are becoming more and more obvious. “In our case, we don’t have to decide where the customers are and where the feedstock is,” he said, noting that a majority of the U.S. population is within a day’s drive of West Virginia. “We need a shining bright new image that shows that.”

Many of the conference attendees also spoke in support of the Appalachian Storage and Trading Hub and the supporting pipelines needed to move the product to markets. Mike Graney, head of the West Virginia Development Office, pointed to the new polyethylene cracker plant under construction in Butler County, Pennsylvania, which is the biggest project in Pennsylvania since World War II and has one of the world’s longest supply trains on site supporting the construction effort. He said there’s enough gas in the region to support five of these facilities, which convert natural gas into pellets that can be used for manufacturing a wide variety of products. Another cracker plant worth $10 billion is in the works in Ohio as well. “We’ve got attractive states for industrial development,” he said.

Citing sources such as The Cato Institute think tank, financial services company Moody’s Corporation, the state development office’s own findings and others, Graney said West Virginia has seen $5 billion in investments since 2017, has a better business tax climate than any of its surrounding states, has the nation’s lowest turnover rate in manufacturing, has the 11th lowest cost of doing business, has no business franchise tax and has a strong rainy-day fund. Some of that investment is already taking place. Frank Bakker, CEO of US Methanol, said his company is in the process of dismantling two of its facilities in Brazil and Slovenia and relocating them to West Virginia. “What is methanol? It’s alcohol in its purest form,” Bakker explained. “You can drink it … you’ll go blind and die … but there are lots of uses for it.” The largest use of methanol is in manufacture of other chemicals, which is why US Methanol is establishing itself in Kanawha County to be close to both the local petrochemical industry and accessible, abundant natural gas that can be converted to methanol.

Other applications include laboratory solvents, antifreeze and vehicle fuel. A small amount of methanol can be added to wastewater to provide a food source of carbon for the denitrifying bacteria, which convert nitrates to nitrogen to reduce the denitrification of sensitive aquifers in some wastewater treatment plants. Challenges to further developing the storage hub and the economic goodies that come with it include a lack of flat land for construction, as well as a lack of cohesive strategic planning. However, Graney said these are issues that can be overcome. “I say we can overcome all of that if we have the right attitude,” he said. “West Virginia is not only wild and wonderful and beautiful. It is a powerhouse.” Kandel said it’s also a matter of properly informing those at the top of large companies around the world what the Appalachian region is capable of.

During the second annual Take Me Home Country Roads Conference, organized by the Morgantown Area Chamber of Commerce in conjunction with the Pittsburgh Chapter of the Society of Professional Services, West Virginia High Technology Foundation President James Estep said the state’s knowledge economy is being enhanced by the transition of federal government operations out of the crowded Washington, D.C., metro area. “The cost of operations there has become astronomical. It just doesn’t make business sense to stay there,” Estep said, referring to Northern Virginia and Western Maryland. “It can be transformative not only economically but cement in place a knowledge sector that could be an example for the whole country.”

An example of this in action is tech company Leidos’ work with NASA and the National Energy Technology Laboratory. In fact, this prompted the firm to start building a whole new campus at Monongalia County’s West Ridge development off Interstate 79. Estep said that as federal functions move to a new area, companies to support those functions also move into the area to go where the work is. He said this often leads to a ripple effect where companies branch out and expand their operations to keep up with demand, creating more jobs in the process.

Comments Off on 8,000 Jobs Added Within Past Decade in North Central WV

North Central West Virginia continues to lead the state in economic progress, according to local experts.

Although many other areas of the Mountain State lag behind national averages in most major economic indicators, the North Central region has continued to thrive and grow, according to John Deskins, director of the West Virginia University Bureau of Business and Economic Research.

“North Central West Virginia is more stable than the nation, it seems. Or, at least, the patterns of the last couple of decades have indicated we have greater stability,” Deskins said. “The region’s economy is very resilient. Part of that depends on the fact that we have some really important federal employment in the region; we have the university in the region; and we have a lot of health care in the region. Those sectors of the economy tend to be really stable,” he said.

The Bureau of Business and Economic Research recently released a study analyzing the NCWV region’s economy over the past few years and looking ahead to expected economic performance through 2023, Deskins said. Businesses in Monongalia, Marion, Harrison and Preston counties added more than 8,000 jobs between early-2010 and mid-2018, resulting in cumulative growth of more than 7 percent, according to the study.

In Harrison County, many of the new jobs can be attributed to rebounding natural gas production and natural gas pipeline infrastructure under construction, Deskins said. “That’s actually something that’s creating benefits in other counties in the state as well, not just the North Central region,” he said. “But definitely the construction projects that have been going on have definitely helped employment and a whole host of economic measures here in North Central.,” he said. “There is lots of stuff going on with the pipeline construction. That’s in Harrison County, and it’s affecting other parts of our region, as well.”

Sherry Rogers, executive director of the Lewis County Chamber of Commerce, said Lewis County has also experienced positive economic gains over the last year, mainly due to increased natural gas pipeline construction in the area. “There are some businesses that have seen an increase in their revenues due to the pipeline and the influx of pipeliners coming to the area and staying in the area,” she said. “Our retail and our restaurants have seen an increase due to that.” Several new businesses have recently opened their doors in and around Weston, Rogers said. “Here in Lewis County we have thriving entrepreneurship,” she said. “We’re comprised mostly of small businesses and we have some exciting new businesses that have opened that have opened this year or are opening.”

These include a retail shop in downtown Weston, a newly opened restaurant and a distillery, MannCave Distillery, Rodgers said. Patricia Henderson, director of the Taylor County Development Authority, said her county’s economy remains stable, partially do to continued coal mining activity. “Right now we are similar with the other areas in the state,” she said. “We do have a coal mine here, and that’s certainly helping us. Leer Mine still producing and moving a lot of coal through the railroad.” The county hopes to attract more oil and gas related companies to settle in the Taylor County area, Henderson said.

“We are trying to attract new businesses, and like all the other counties throughout the state, we are trying to recruit some of the oil and gas into our county,” she said. “In 2018, we had some property that the development authority marketed, and we did have an oil and gas company purchase that property to build some of their field offices. So we’re excited about that. That is a three-year plan.”

Taylor County recently became the recipient of a grant that will be used to perform a broadband internet study, Henderson said. “One of the problems that we hear a lot is the fact that we don’t have high speed internet in a lot of the areas of our county,” she said. “So we’ve got a grant to do a study that will help us to asses our needs and see where our underserved and unserved areas are so we can identify them. Then we can potentially go after some federal funds to help with that.”

Monongalia, Preston enjoy hotel occupancy spike that beats even state’s solid year

As West Virginia tourism officials celebrate increases in hotel occupancy, the numbers in Monongalia and Preston counties outpace even the state’s rise. Gov. Jim Justice recently touted a 16.1 percent increase in statewide hotel occupancy comparing June 2018 to June 2017. The local area has enjoyed a 17.9 percent hike in that same comparison, said Susan Riddle, executive director of the Greater Morgantown Convention and Visitors Bureau.

“We put a pedal to the metal since the beginning of last year, and we haven’t looked back,” Riddle said, adding that she can look at any month and see an upward trend in bookings. Justice also said there was a 20 percent revenue increase in a year-over-year comparison to June 2017. In Mon and Preston, revenue was up 20.2 percent June over June. Every region of the state has seen increases, Justice said, with the first two quarters of 2018 showing hotel occupancy up 11.7 percent, with revenue growth of 14.9 percent.

“One of my first decisions in office was to launch a new tourism campaign that would spread that message like never before,” Justice said July 25. “West Virginians should be proud of what we’ve done here, because it takes all of us, telling our story and rolling out the welcome mat, to make this happen.”

“From day one, the governor had a vision for what could happen with West Virginia tourism,” said state Tourism Commissioner Chelsea Ruby. “The success we’ve seen this year is a direct result of that vision and the governor’s commitment to growing our tourism industry. Tourism means jobs, and the numbers that the governor released today translate into more West Virginians working in a sector that still has enormous room to expand.”

STR, a global hotel research company, reported the statewide hotel occupancy rates. In Mon and Preston counties, there has been a significant increase since January 2017. Riddle said that means jumps in all categories from occupancy to revenue to demand. Mon and Preston have 28 lodging properties combined, resulting in 2,600 rooms available daily. Filling up those rooms with travelers generates sales tax dollars.

“We target everything we do. Our mission is one more night, one more dollar. It’s as simple as that. We don’t need to make it any more complicated,” Riddle said. “For every $100, CVB receives $3. It’s not just about people spending the night to go ahead and generate lodging tax, it’s what are they doing while they’re here.”

That entails looking at the four types of tourists Riddle claims frequent this area:

Adventurers and explorers (the largest group),

attendees,

planners

and relaxers.

“For us, our big draw, we have a synergy that is the combination of a lot of different benefits,” Riddle said. “We sell our region. We connect our local area with our audience.”