Comments Off on Reflecting & Projecting – Observations from 2025, Projecting BDR’s Best Year in 2026

Commercial Real Estate Outlook: From Soft Growth to Renewed Momentum in 2026

Economic growth in the United States remained relatively soft throughout 2025, with uneven GDP performance and constrained job expansion contributing to cautious investor sentiment. Despite this, leading indicators suggest that a combination of lower interest rates and improving market fundamentals should spark increased activity in 2026. After a prolonged period of elevated borrowing costs, anticipated rate cuts are expected to make capital more accessible, igniting deal flow and investment confidence across sectors. Recent industry projections signal a meaningful shift in market trajectory.

Global commercial real estate powerhouse CBRE—the largest brokerage firm of its kind in the world—recently projected that commercial real estate sales volume will grow at a 5.7% compounded annual rate from 2026 through 2029. This forecast not only reflects renewed transactional activity but also underpins what many analysts view as a transition from the recessionary phase of Mueller’s real estate cycle into expansion territory for most property types, though not all sectors will participate equally.

Office Market: Signs of Improvement in Deal Flow

After years of subdued activity, deal flow in the office sector improved modestly in 2025, particularly within Class A and Class B space. Notable transactions included the leasing of 65 Professional Place and a significant long-term lease at 150 Clay Street, among others that helped stabilize sentiment in office markets traditionally strained by vacancy and changing workplace dynamics. In 2025, BDR closed 106 deals (58 lease and 48 sale). 38 of those deals were of the office sector. View our closed transactions page for the full list.

These improvements build on broader market indicators showing narrowing vacancy rates in higher-quality assets and rising lease demand relative to recent troughs, especially as tenants chase well-situated and amenitized office space. While legacy Class C office properties still lag, the inflection in Class A and B metrics points to early stabilization.

Investment Appetite Strengthens

Investor confidence has strengthened on the back of several positive catalysts:

Lower interest rates now on the horizon are expected to reduce borrowing costs and stimulate acquisition activity. Business Insider

Bonus depreciation provisions and enduring tax advantages keep real estate competitive as both a wealth-building and wealth-preservation tool.

Improving fundamentals in sectors like industrial, multifamily, and prime office space support continued capital inflows.

Although cap rates have risen modestly in tertiary markets we serve, reflecting risk premiums and market recalibration, the outlook for 2026 anticipates cap rate compression of 25–50 basis points as borrowing costs decline. That said, cap rate trends will remain sensitive to local supply-demand dynamics within each sector, underscoring the importance of targeted underwriting and market selection.

Construction Activity Remains Limited

New construction starts continued to lag in 2025, a trend expected to persist into 2026. According to industry reports, construction costs have risen roughly 39% compared to a 27% inflation rate over the same period, exerting upward pressure on project budgets and timelines. Meanwhile, labor shortages—driven by an aging workforce, fewer new entrants, and restrictive immigration policies—have further constricted capacity. As a result, new construction projects are at multi-decade lows, with limited starts anticipated in 2026 given cost and complexity challenges. (Source: CRE Daily analysis.)

Geopolitical Tensions and Tariff Uncertainty

Policy developments in recent years, including tariffs instituted under President Trump’s strategy, contributed to challenging geopolitical relationships and broader market uncertainty. These dynamics led some investors and occupiers to adopt a cautious “wait and see” approach as markets absorbed the implications of trade policy shifts. While tariffs are expected to recede somewhat as a focal point in 2026, geopolitical tensions—heightened by events such as the recent developments in Venezuela and other regions—will continue to exert subtle pressure on capital flows and investor risk appetite.

Youth Sports: A Surging Real Estate Engine

One of the most dynamic and under-recognized drivers of real estate activity is the youth sports and tournaments industry. Now estimated as a $36 billion sector projected to balloon to $260 billion by 2034, youth sports represent nearly 20% annualized growth, creating robust demand for purpose-built facilities and ancillary development.

This trend is evident in a number of regional projects attracting teams, families, and associated commercial activity, including:

The Bridge in Bridgeport, WV – a multifaceted youth sports and event venue stimulating local hospitality and retail demand.

Mylan Park in Morgantown, WV – a community-anchoring sports complex drawing significant regional visitation.

Hagerstown Field House in Hagerstown, MD – a facility packed with action for all ages—from soccer, basketball, and flag football to lacrosse, volleyball, and more.

Berkeley County Sports & Event Centerin Martinsburg, WV – a 256-acre facility that will be recognized as an elite tournament quality sports, fitness and recreation venue, serving athletes, coaches and fitness enthusiasts of all ages and abilities.

Youth sports campuses are becoming major placemaking assets, driving foot traffic, hotel stays, restaurant patronage, and broader economic spillover — reinforcing real estate’s role at the intersection of community and commerce.

Taken together, these trends suggest that 2026 represents a pivotal reset for commercial real estate rather than a return to pre-pandemic norms. Improving capital markets conditions, disciplined new supply, and selective demand growth are laying the groundwork for a healthier and more sustainable expansion phase of the real estate cycle. While geopolitical uncertainty and sector-specific challenges remain, investors and occupiers who stay focused on fundamentals, local market dynamics, and long-term demographic drivers will be best positioned to capitalize on the next wave of opportunity. As confidence rebuilds and liquidity returns, commercial real estate is poised to reassert its role as a durable engine for value creation and economic growth.

Article written by David Lorenze, Principal/Associate Broker

Comments Off on Reflecting and Projecting 2023 – 2024

As humans, it is natural for us to take things for granted. Our children will stay young forever. A business will continue on its current growth trajectory. 2023’s rapidly changing interest rate environment served as a reminder that things can change quickly. On March 17, 2022, the federal government set out to slow down an economy that was growing at an unsustainable rate. The federal funds rate rose from 0.25% to 0.50% in March 2022 to 5.25 to 5.50% on July 26, 2023 which represents the last rate hike (https://www.forbes.com/advisor/investing/fed-funds-rate-history/). That’s 500 basis points in 16 months! Rapidly increasing the federal funds rate achieved the government’s goal of slowing inflation. The speed of change was rapid, being the fastest in multiple decades, and sent shock waves throughout the commercial real estate world. Some of Black Diamond Realty’s observations are captured in the bullet points below.

Buyers were forced to adjust their internal underwriting to account for higher borrowing costs, due to higher interest rates, which ultimately led to rising cap rates.

Sellers are also forced to adjust value expectations when evaluating their assets and pricing to meet required DSC for Buyers of their assets (making it a bankable deal). Sellers are slow to adjust to a changing economy. Human nature protects our psyche resulting in most sellers reluctancy to accept the fact that asset valuations from mid-2022 are no longer an accurate representation of today’s market value.

The buyer-seller gap was wide at the beginning of early 2023 but slowly shrunk. Like many things in life, time heals wounds or, in this case, narrows the buyer-seller value expectation gap.

Banks are quick to adjust pricing and risk tolerance guidance and adjust required DSC levels and reprice assets.

Banks struggle with nonperforming assets and collections.

Metro markets often rise faster than tertiary markets and, therefore, tend to fall faster when economic conditions adjust. The markets Black Diamond Realty services experienced a slowdown in activity but it was much less profound than many metro markets consuming national media.

Greater increase in creative deal structures including seller financing.

Higher interest rates make leasing a more attractive option for some businesses. In comparison to sale volume, leasing activity has experienced increased transactions across most sectors of commercial real estate.

High borrowing costs, combined with increased labor and material costs, have resulted in a significant slowdown in new construction starts. This is a national trend in most markets.

Land sales have slowed. Higher interest rates and increased construction costs make it more difficult to “pencil” returns that meet developer hurdle (internal return) rates.

Less individuals can afford to buy their “dream home” because of rising home prices and rapidly changing interest rates which has resulted in many potential buyers sitting on the sidelines and renting longer. Market rents have continued to tick up in most markets helping to create greater demand in CRE’s multifamily sector . Market inventory continues to be the key struggle leading to lower transaction volume this sector.

2023’s theme was rapid change. What will 2024 look and feel like? Predicting the future is impossible, but national trends and experience allow us to make educated guesses. Please bear in mind you should always complete your own due diligence before making an investment decision. Black Diamond Realty’s 2024 predictions are as follows:

The Federal government is anticipated to lower interest rates three to six times throughout the year. BDR anticipates four lowering events with a final result between 100 to 150 basis points.

Election years usually create uncertainty and fear which causes many investors and businesses to adopt a holding pattern. Declining interest rates should create a market buzz but uncertain political outcomes will soften 2024’s activity. In comparison to 2023, greater CRE deal volume is anticipated.

Combined with high bank CD and money market rates, 2023’s slowdown in CRE activity has led to pent up demand with a lot of “powder” sitting on the sidelines. Cash is, once again, king/queen. “One person’s demise is another’s potential treasure.” Many adjustable and/or maturing loans will present buying opportunities over the next 12-24 months.

Banks will be quick to move nonperforming/uncollectable assets off their books. This will create opportunities for buyers to pick up properties at a discount…timing and connections will be key to buying up these assets.

Office assets, overleveraged real estate and properties financed with short-term debt all face headwinds in 2024. Distress, leading to buying opportunities, is anticipated across these categories.

User demand for industrial/logistics, retail and residential is anticipated to remain strong.

Cash buyers and international investors are anticipated to be more prevalent.

Banks will continue to tighten their lending belts and stress properties at higher interest rates (8-9%). Debt service coverage ratio (DSCR) levels will continue to be higher than pre-COVID levels. Most banks will require a 1.25 DSCR

We often joke Black Diamond Realty is not a group of magicians. We are skilled CRE professionals whose job is to maximize exposure, navigate complicated processes and provide sound consultative investment and decision-making guidance based upon experience. We are in the commercial real estate trenches every day. We do not sell homes.

Diversifying investments, pursuit of passive income, filling a void in your portfolio’s performance (leasing) and liquidating an asset to meet long-term goals are all reasons to contact our Black Diamond Realty team. Call our team of experts today to set up a consultation. We look forward to serving you in 2024 and beyond.

Article by:

David Lorenze, CCIMPrincipal, and team.

Comments Off on Reflecting and Projecting 2022 – 2023

Congratulations! You just rode one of the wildest rollercoasters the modern economy has ever experienced. Roughly one year ago, experts predicted interest rates would begin ticking up twenty-five to fifty basis points, with a target of 4.5 to 5% interest rates. The goal was, and still is, to fight record high inflation (9.1% in June 2022; a 40-year high). Many projections were far off, including ours. In today’s market, a 4.5 to 5.0% interest rate on a deal is unheard of and would make investors drool. As we enter a new year, we are looking at the prime rate hovering in the mid sevens; that’s 7.5%! This marks a 400-basis point increase in the past nine months.[i] Last year experienced the most aggressive economic tightening campaign in over three decades. So, how does that affect commercial real estate?

Rising interest rates put downward pressure on valuations. Financial institutions, including regional and national banks, typically want to achieve a 1.20 to 1.25 debt-service coverage ratio (DSCR), meaning 20%-25% of a project’s cash flow is available to pay current debt obligations. When the cost of borrowing funds increases, meeting required DSCR ratios is more difficult, and a buyer cannot afford to pay as much value to a seller while still maximizing leverage (borrowing power). A buyer either has to come up with more capital to lower the loan-to-value (LTV) ratio or lower the offer price. Here is an example:

ABC Investment LLC has renovated an asset and wants to cash out to redeploy capital into the next project. You like the asset a lot. You offer full asking price – $1,250,000. A bank that requires an 80% LTV ratio (some banks will offer lower, say – 70-75% LTV) will result in you needing to borrow $1,000,000. Nine months ago (Q2 2022), you could have hypothetically achieved an interest rate of 3.65% (Black Diamond often saw rates between 3.25% to 4.00%). Amortizing $1,000,000 over 20 years at 3.65% interest results in a monthly payment of $5,876.97. Fast forward nine months (Q1 2023), and that same loan structure has changed drastically.[1]

As of December 15, 2022, the current prime rate is 7.5% in the U.S., according to The Wall Street Journal’s Money Rates table, which lists the most common prime rates charged throughout the U.S. and in other countries by averaging out the prime rate from the ten largest banks in each country. The federal funds rate is currently 4.25% to 4.50%. With that in mind, you can see how the “fed funds plus 3.00” rule of thumb plays out: 3.00% + 4.50% = 7.50%.[ii] At Black Diamond Realty, we would argue this rate is very conservative, as our experience has resulted in many regional banks willing to entertain deals at lower interest rates – with a 250 to 300 basis point spread in play.

Getting back to our example, your investment company’s new interest rate (7.25%; 275 basis point higher than federal rate) results in a monthly expense of $7,903.76. The difference between a 3.65% interest rate and a 7.25% interest rate is $2,026.79/month. The yearly difference is $24,321.48. In today’s market, let’s assume a regional multi-family asset comps out and sells at a 7% capitalization rate. Utilizing a 7% capitalization rate, the $24,321.48 yearly interest rate difference results in a downward value adjustment of $347,449.71 ($24,321.48 / 0.07). This ~$350K difference results in a seller/buyer “value gap.” Buyers are forced to react quickly because the capital markets respond within weeks, often days. Some buyers are struggling to find deals while sellers reassess their motivations to liquidate. Sellers are realizing they missed the market peak. Buyers are coming to the table with greater liquidity to meet DSCR (healthy, “bankable” deal) and bridge the seller gap.

The current market reflects the seller-buyer gap. On its own, this would be bad news for sellers everywhere. Fortunately for the market, supply and demand also comes into play. Like many things in our economy, construction materials (think Lowe’s, Menards, Home Depot) have experienced significant inflation in 2022. Construction expenses rose 13.7% since September 2021.[iii] Higher construction expenses, including excavation work, have resulted in lower nationwide new housing construction starts. Privately-owned housing starts in November were at a seasonally adjusted annual rate of 1,427,000. This is a 0.5 percent below the revised October estimate of 1,434,000 housing starts and is 16.4 percent below the November 2021 rate of 1,706,000.[iv]

The same trend is true across most sectors of commercial real estate. Higher material costs combined with higher costs of borrowing funds (interest rates) has resulted in a slowdown of new construction activity. We anticipate this trend to continue. Sticking with the multifamily sector, lower housing starts have resulted in increased rents and corresponding increased valuations. The same data shows a downward trend in construction costs during Q4, 2022 which is something to watch in 2023. So, what else can we expect in 2023?

Deals happen in all cycles of commercial real estate. Rising interest rates create downward pressure but, on the flip side, rising rents/income result in higher valuation. Do these two opposite effects counterbalance each other? The answer is specific to each commercial real estate sector (supply/demand) and the specific market. Depending upon the market, rising income is outpacing inflation which continues to push rents higher. The risk lies in the job market. Job loss and higher unemployment will eventually reduce consumer purchasing power and result in less demand for materials, goods and real estate. When unemployment rises, rent growth will be at risk for most sectors of commercial real estate. Our team is keeping a close eye on unemployment in 2023.

The ‘R’ word has been tossed around many dinner tables and watering holes across America. An economic recession occurs when GDP, which measures trade and industrial activity, declines in two successive quarters. Are we amid a recession? US Government courses reported that Quarter 3 of 2022 saw a 3.2% increase in GDP over the previous quarter.[v] This increase is welcoming news after two quarters of declining GDP. Some fear the data is artificially inflated due to the government’s easing of energy costs. The biggest challenge in reviewing federal government data is the lag. Most data lags at least three months, sometimes six, which means the Fed is making decisions based upon outdated information. What does the real estate market cycle forecast look like knowing this? Keep reading.

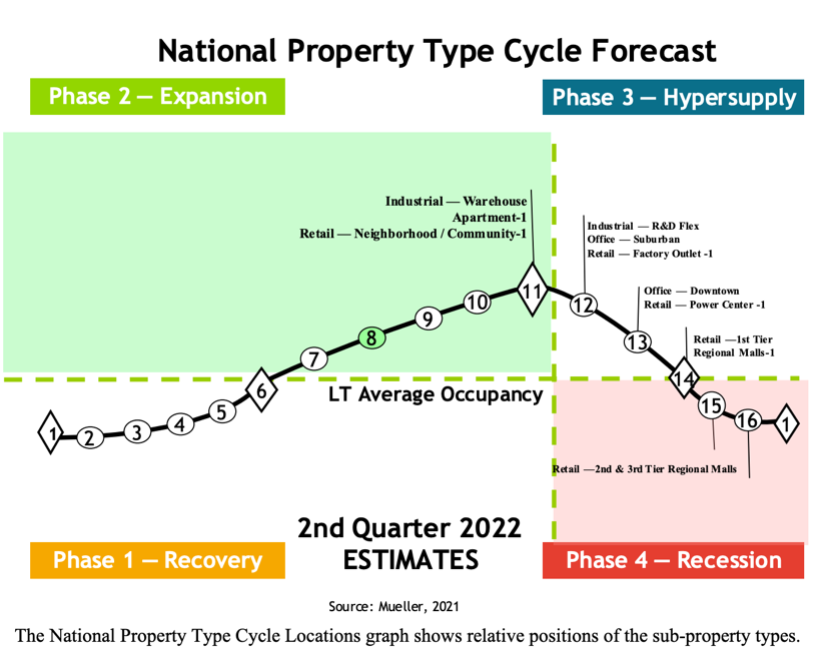

Real estate market cycles vary by sector and location, amongst other factors. Mueller’s[vi] forecasting model breaks down the real estate market cycle into four phases:

There are 16 total points along the horizontal axis. Points 1-11 are in phases 1 and 2 which represent a period of growth. Points 12-16 are in phases 3 and 4 which represent a period of decline. The four market cycle quadrants have varying characteristics. Phase 1, Recovery, is characterized by declining vacancy with little to no new construction. Negative rental growth to below inflation rental growth is expected during this part of the cycle. Phase 2, Expansion, is characterized by declining vacancy with greater new construction. High rent growth is common. Phase 3, Hypersupply, is characterized by increasing construction with continued and/or increasing construction. Rent growth remains positive but begins to decline. Phase 4, Recession, experiences increasing vacancy with more completions. Below inflation and negative rent growth is experienced during this part of the cycle. The Mueller report’s primary objective is to enhance investment decision analysis – to make investors aware of national trends.[vii]

Sector breakdowns are provided in the bullet points below with quick comments about the regional market. Keep in mind what is happening in New York City, NY is not necessarily a direct correlation to what is happening in Bridgeport, WV; hence several anecdotal comments from Black Diamond Realty’s perspective which are focused on the two core areas we serve: North Central WV and WV’s Eastern Panhandle. We recommend referencing the chart as you review the points below. Mueller’s data is the black bullet points. Black Diamond’s points are white sub-bullet points. In addition to this distinction (national trend – Mueller vs. Black Diamond), bear in mind Mueller’s chart lags by two quarters. The cycle has progressed along the bell curve over the past three to six months.

Point 11: Peak of Phase 2 – Expansion Cycle

Industrial – Warehouse

Remains strong throughout north central WV and WV’s Eastern Panhandle. For north central WV, keep an eye on oil and gas volatility/strength in 2023. For WV’s Eastern Panhandle, we are watching consumer confidence and retail strength.

Apartment

Remains strong in both markets due, in part, to the ability to push rental rates to counteract rising interest rates.

Retail – Neighborhood/Community

Still demand albeit at a slowing pace in both markets. Headwinds are forming which we believe will negatively affect all subsectors of retail.

Point 12: Beginning of Phase 3 – Hypersupply

Industrial – R&D Flex

Flex space has remained strong in both markets. North central WV has an undersupply of quality, newer flex space with docking capability. The Eastern Panhandle has consistently filled any new supply but it appears some headwinds could be forming (Hypersupply phase) where new product is taking longer to secure tenancy.

Office – Suburban

Demand still exists albeit at a slower clip compared to pre-Covid.

Retail – Factory Outlet

Point 13: Middle of Phase 3 – Hypersupply

Office – Downtown

Major metro markets have struggled post-Covid. In smaller/tertiary markets, he jury is still out on whether long-term leases will restructure plans as

Predicting future trends is nearly impossible. Market dynamics are complex and can shift quickly. Our team of experts has made some observations and anticipations for 2023. In no way, shape or form are we suggesting these “educated guesses” to be fact. Mere predictions are not indicative of actual future results. Please consult with your professional legal and financial advisors, complete your own due diligence and draw your own conclusions pertaining to the best financial moves for you.

Black Diamond Realty Predictions:

Real estate is considered by many as a great hedge against high inflation and a strong diversification play. Income producing assets are still warm, not hot, as an investment diversification play. Activity has cooled due to higher interest rates putting downward pressure on valuations. Ranking the sectors is difficult because there are so many factors (location, age, tenant, traffic patterns, surrounding amenities, etc.) but anticipated trends can be projected. In addition, there are several macroeconomic and microeconomic items we anticipate playing out in 2023.

Multifamily and industrial are anticipated to remain strong in the markets we serve. However, look for headwinds beginning to form within 12 to 24 months. Office is the weakest sector as evidenced by higher-than-average historical vacancy rates caused by lower demand created, in part, by work-from-home trends.

Tertiary markets with a core employment base of eds, meds and government jobs (considered recession resistant) will become more attractive to outside investors who are seeking a “safe place” to park capital. West Virginia has significant positive momentum as evidenced by the numerous basic employment announcements throughout 2022. Tertiary markets, similar to several growing areas in West Virginia (North Central, Eastern Panhandle), offer higher cap rates which are attractive to investors. Review Black Diamond Realty’s October newsletter article which compiles numerous statewide job announcements. Click Here.

One to two additional rate hikes in the first half of 2023. We anticipate a reversal, declining rates, starting as early as Q3 or Q4, 2023.

Can the government continue to service its debt at high interest rates? An economist who follows monetary policy, politics and global business much closer than our team will need to answer that question. What we know about monetary policy and our government’s current debt obligations is concerning, at best – downright frightening to others.

Black Diamond Realty anticipates seeing debt options with lower LTV ratios in 2023. Banks will adjust from offering 75-85% LTV to a range of 70-80% LTV.

Construction starts will continue to slow in most sectors. Multifamily and industrial may continue to expand in 2023 but high interest rates are putting downward pressure on construction starts.

Consumer confidence will slip. Challenging retail financial reports will follow. There will be heightened volatility in the stock market.

Our belief is that we are in the midst of a recession. It is either already here or quickly approaching. Government data lags by several months. Consumer confidence has declined during 2022.[viii]Inflation reached record highs in 2022 although it has been declining in recent months. Some believe the inflation decline is, in part, artificially enhanced by the government’s proactive action in releasing 1 million barrels per day of oil reserves. Energy prices will remain volatile especially if/when this strategy is lifted.

Black Diamond Realty is keeping a close eye on unemployment. When unemployment rates increase, consumer purchasing power will decline which will have a trickle up effect to GDP, negatively influencing most sectors in commercial real estate (most notably, retail).

For Black Diamond Realty, sales volume is forecasted to decrease while leasing volume will increase which should lead to leasing price increases in the high demand sectors (industrial and multifamily).

We recommend each party consults with its professional accountant, tax, and legal advisors to better understand the effects of market conditions and real estate transactions. Primary keys to successful investments are knowing the market, the numbers and market trends. Our professional team at Black Diamond Realty is an industry leader. Our company mission is to add value to the communities we serve. We look forward to consulting with you in 2023. Make it a successful investment year.

[1] It should be noted that interest rates can change drastically depending upon many factors, including the deal’s strength, the borrower’s financial strength (including investment and business experience), debt-to-liquidity ratios, and LTV.